The purpose-built student accommodation (PBSA) sector is continuing to grow despite the huge impact on universities from the coronavirus pandemic, which has seen the vast majority close their doors and most students returning to their hometowns to be in lockdown with their families.

The latest data from StuRents indicates that, as of June, almost 23,000 PBSA beds are being advertised for the 2020-21 academic year.

Assuming all schemes in the pipeline that are currently being marketed do come to fruition this year, then the PBSA market could exceed 700,000 bed spaces for the first time, with private operators controlling more than half of supply.

Additionally, with approximately 80% of developments in the pipeline likely to be managed by private enterprises, the share of accommodation managed by universities is set to shrink even further in the coming years.

StuRents says that, whilst the total number of new beds currently equates to year-on-year growth in all PBSA supply of 3.4% (2019: 5.5%), the final figure is likely to change between now and the start of the academic year.

When split by accommodation type, private PBSA is currently anticipated to grow by 5.7% year-on-year, whilst university accommodation is set to increase by 1.1%.

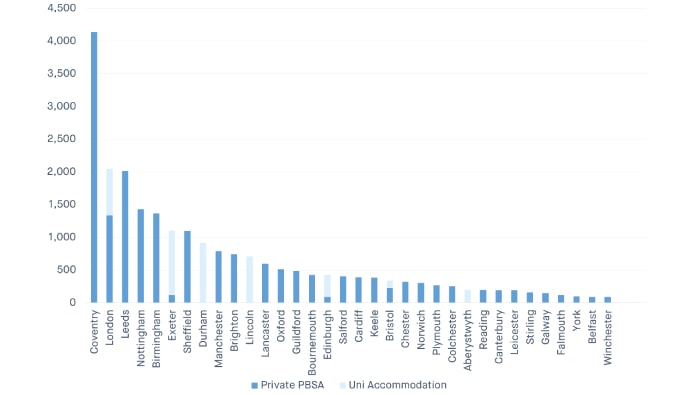

Figure 1: New PBSA beds by location & type (2020-21)

Understandably, some developers have decided in the current climate to postpone the delivery of new schemes, thereby cutting the number of developments that will become operational this year. This includes the decision by Unite Students to preserve cash by deferring the delivery of two schemes set to be built in London and Bristol.

In a similar fashion, Empiric Student Property has sought to conserve cash during a time of uncertainty by pushing back the delivery of three developments until market conditions stabilise. These schemes include Emily Davis in Southampton, a refurbishment project in Canterbury, and St Mary’s in Bristol, with a combined total of 519 beds.

Watkin Jones, by contrast, is still planning to deliver a total of six schemes by Q3 2020, with a seventh due to be complete in Q4 2020.

Some of the largest schemes being marketed for 2020-21 include the huge 1,023-bed Onyx development in Birmingham, as well as the 976-bed White Rose scheme in Leeds. The former is to be managed by Fresh Student Living, whilst the latter is set to be operated by Unite Students.

Elsewhere, over 4,000 beds have been earmarked for delivery this year in Coventry, a market that is highly exposed to a drop in international students.

In London and Leeds, meanwhile, over 2,000 units are due to hit the market, whilst Nottingham is set to receive over 1,400 new beds.

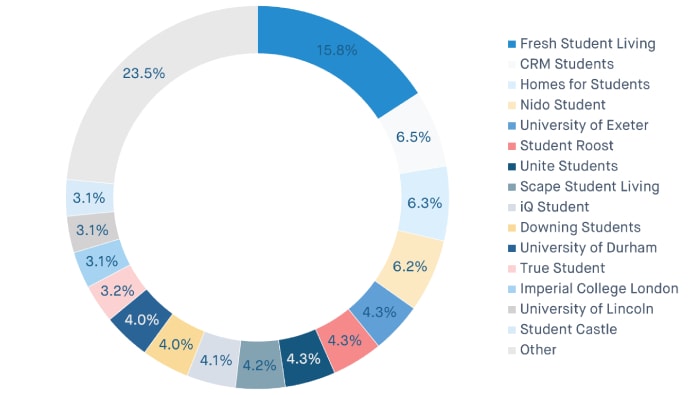

From an operator point of view, Fresh Student Living is to manage the largest share of new beds, with its total equating to more than twice as many as CRM Students in second place.

Figure 2: New PBSA beds by operator (2020-21)

It is still largely unknown what the true impact of coronavirus will be on full-time students, which means new supply entering the market will find itself in a ‘truly unique and therefore challenging environment’.

“Understanding how supply is likely to change for 2020-21 as well as the underlying seasonality within a given location, can help operators make more informed decisions regarding their marketing strategy for the new academic year,” StuRents concludes.

*All charts provided by StuRents

.png)

.jpg)

Join the conversation

Be the first to comment (please use the comment box below)

Please login to comment