This comes despite the annual volume of all residential housing transactions across England and Wales falling from 1,194,025 in 1999 to less than 868,886 in 2018.

Prime market growth holds steady in the past five years

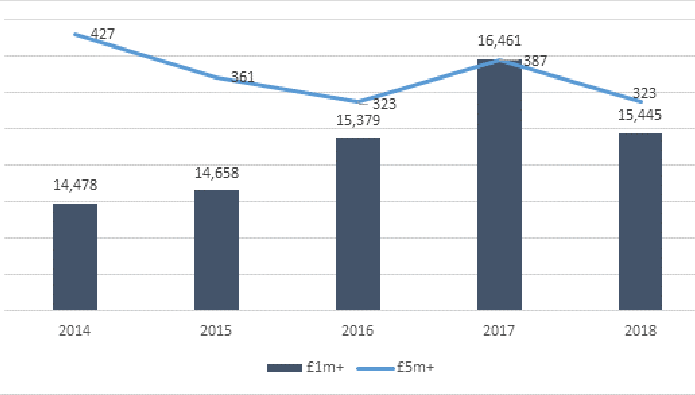

Despite rumours of a prime market slowdown, Private Finance’s analysis suggests an overall trend of growth over the past five years, with increases in the number of £1 million-plus property transactions every year except 2018.

Sales in the £5 million-plus bracket have been more volatile but have held above 320 for the past five years.

The graph below shows the annual volume of residential housing transactions between 2014-2018:

Average UK house prices up by 189% since 1999

Private Finance says the rapid growth in prime property transactions over the past 20 years is largely due to increasing house prices over this period.

The average UK house price was just £80,443 in 1999, compared to £232,710 in July 2019 – a 189% increase in nominal terms.

Interestingly, the top five most expensive areas in the UK have remained broadly unchanged, with Kensington and Chelsea retaining the top spot in both 1999 and 2019, though average house prices for each area have undergone significant changes.

In Kensington and Chelsea, for example, the average house price has risen from £309,698 to £1,295,861 – a percentage increase of 318%.

Mortgage rates plummet as borrowers benefit from low-interest environment

Though the UK property market has become undoubtedly more expensive in the past two decades, average mortgage rates have become far more affordable.

For instance, the average two-year fixed rate at 75% loan-to-value (LTV) in 1999 was 6.19%. This rate is now as low as 1.64%. Similarly, a five-year fixed deal at 75% is now just 1.92%, compared to 6.64% in 1999.

This makes servicing a prime property mortgage more viable. A homebuyer purchasing a £1 million home with a 25% deposit would pay £4,920 per month if on a two-year fixed mortgage deal in 1999. Today, the same monthly payment would fall to £3,049 – a saving of almost £2,000, according to the broker.

“The housing market has undergone a radical transformation, with average house prices in particular almost unrecognisable,” Simon Checkley, managing director of Private Finance, comments.

“Transactions of houses in higher price brackets have soared in accordance with rising prices, creating a much bigger and more complex prime market.”

He adds: “Though activity in the housing market this year has been subdued, the prime market remains supported by years of consistent growth. Less activity is to be expected given the ongoing political and economic uncertainty affecting the country, which has impacted the number of prime transactions in the capital in particular.”

However, Checkley says once Brexit has reached its conclusion, we may see ‘a rush of pent-up demand as the spectre of uncertainty is at least somewhat removed’. UK prime property will continue to be an attractive prospect for overseas buyers, and domestic buyers will be looking to get their property plans back on track.

“Independent mortgage advice is vital for prime buyers who often have complex income structures and, with such high values of stake, could skim thousands of pounds off their monthly repayments by selecting a competitive deal,” he concludes.

.png)

Join the conversation

Be the first to comment (please use the comment box below)

Please login to comment